You must have read media reports about how credit card customers received email/SMS messages about fraudulent transactions done on their credit cards from foreign locations. Did you know that international online transactions on credit cards don’t need a one-time password (OTP)? Hence, if someone gets your credit card details, they can do online transactions from a foreign location, as they don’t need an OTP validation.

So, how can you protect yourself against such misuse or fraud? One of the ways of doing this is by disabling certain transactions and putting limits on others. Let us understand how.

To protect yourself from fraudulent transactions, banks allow you to disable certain transactions on your credit cards. Even if a credit card is lost or stolen, you can limit the damage by putting transaction limits. Here is how to go about doing the same.

Banks give you the option to enable or disable international transactions. When you get a new credit card, by default, international transactions are disabled. If you want to do an international transaction, you have to enable them.

For example, the screenshot above shows how you can enable or disable international transactions on your HDFC Bank credit card. You can control the credit card settings through internet banking or the bank mobile app. You need to log in, go to the credit card section, and proceed to the card limits section. Unless needed for some specific transaction or when you are travelling abroad, it is advised to disable international transactions on your credit card.

Even when you need to do a specific international transaction, you can enable international transactions on your card just before the transaction. On transaction completion, it is recommended that you once again disable international transactions.

When you travel abroad or when you have recurring international transactions on your credit cards, you can control which types of transactions to allow and up to what limits/amounts. With transaction limits in place, even if the card details are compromised, the loss can be limited.

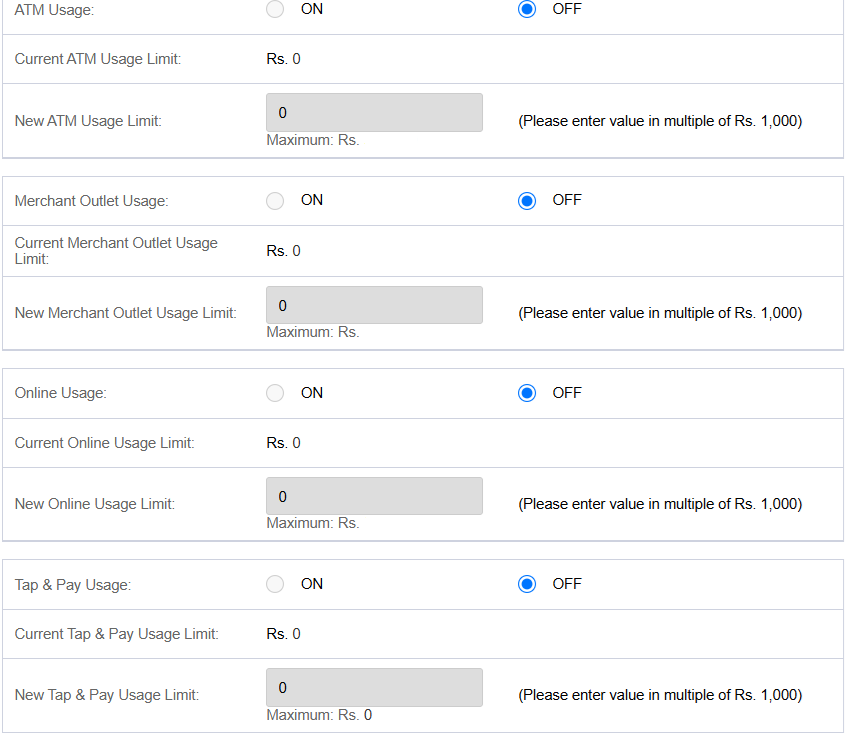

For example, HDFC Bank allows you to control the following types of international transactions on your credit card.

When travelling abroad, it is recommended that you carry a forex card with zero or low forex charges. However, during an emergency, if you plan to withdraw money from an ATM using your credit card, you can enable ATM usage. When you enable ATM usage, you can set transaction limits.

During your foreign travel, you may want to use your credit card for specific transactions at merchant outlets, like paying for meals at hotels or shopping for yourself and family members. You can enable merchant outlet usage for such transactions and set appropriate transaction limits. Any transactions done over the specified limit will be automatically declined.

If you have to make any online purchases or pay for any annual subscription(s), you can enable international transactions. Once the transaction is completed, you can disable international transactions. When you enable online transactions, you have the flexibility to modify the limits by increasing or decreasing them at any time.

Similar to merchant outlet usage transactions, you can enable or disable the tap and pay usage transactions. With tap and pay usage, the transaction can be done by placing the card on the point of sale (POS) machine without the need for inserting it in the POS machine. There is no PIN number required to be entered to complete a tap and pay transaction.

The above image shows how an HDFC Bank credit card user can enable or disable various transactions along with setting transaction limits in HDFC net banking.

Similar to international transactions, you can enable or disable various domestic transactions and set limits for each transaction type, as explained in the above section. You can choose which transaction types to enable or disable. For example, cash withdrawal through credit cards is not advisable as the interest will be charged from the day of withdrawal. Hence, it is recommended that you disable ATM usage on your credit card.

For merchant outlet usage and online usage, you can enable them and set transaction limits. The transaction limit can be fixed based on your past monthly usage. If you have to do an one-off transaction for a higher amount, you can increase the limit for that transaction. Once the transaction is completed, you can reduce the limit.

Some people enable tap and pay usage as it is convenient. However, some people disable it due to security concerns, as no PIN is required to authenticate the transaction.

In the last few years, financial frauds have increased a lot. These involve fraudulent transactions related to UPI, credit cards, debit cards, hacking bank account details, etc. Hence, the government, RBI, and banks have been taking various measures to educate bank customers on how to safeguard themselves and not becoming victims of these frauds.

As a vigilant customer, you should analyse the transaction types for which you use your credit card(s) and enable only those transaction types accordingly. For the transaction types enabled, you should set appropriate transaction limits. The limits can protect you from potentially higher losses in the event of fraud.

For international transactions, as a precautionary measure, you should disable all transaction types unless there is a need for a particular transaction type. For domestic online transactions, you have an additional safety measure of authenticating the transaction by putting in an OTP.

However, for an international transaction, the OTP is not required to complete the transaction. If your credit card details are hacked, they can be used for fraudulent transactions, if international transactions are enabled. Hence, it is better to disable international transactions.

For a one-off international transaction, you must enable international transactions on your credit card. After the transaction is completed, you must disable international transactions again. For recurring international transactions, you must apply appropriate limits.

With the disable and transaction limit features, banks provide customers the control in their hands. As a customer, you should use these features to your advantage. You must disable international transactions when not using the credit card for them.

For domestic transactions also, you should enable only those transaction types that you use and that too with appropriate limits. It will help you safeguard your credit card against potential fraud. Even if a fraud happens, with transaction limits in place, the damage will be limited.

Gopal Gidwani is a freelance personal finance content writer with 15+ years of experience. He can be reached at LinkedIn.